The 2026 Manufacturer Loan Pack: Plant, WC & Property

The RBA cash rate sits at an indicative 4.10% (current at publication) after the March hold, March 2026 PMI printed 49.8 (the first contraction in five months), and the BOQ-to-Challenger equipment finance portfolio sale — publicly reported at approximately $3.7bn — is reshaping the non-bank panel. Most manufacturers are still stacking facilities in the wrong order. The right sequence — plant, working capital, property — decides which application gets approved and which one blocks the next. Here's the 2026 manufacturer loan pack playbook.

One Doc Home Loan: Manufacturer Retained Earnings (2026)

Pty Ltd manufacturer directors routinely get told their paper income doesn't count because it's retained inside the company rather than drawn as director income. On a One Doc home loan the read changes — BAS turnover and a self-declared statement replace the full-doc bank servicing logic. Here's the decoder of where the money actually lives, and which income sources pass or fail the One Doc file.

Sale & Leaseback for Manufacturers (2026): Plant to Cash

Most manufacturers think their owned CNC is locked equity — quietly sitting on the factory floor while working capital gets squeezed by 60-day raw material terms. Sale and leaseback reads the asset differently. The machine stays on the hardstand, the title moves to a funder, cash hits the trading account, and a deductible rental replaces a depreciating lump. Here's the before/after and the lender view.

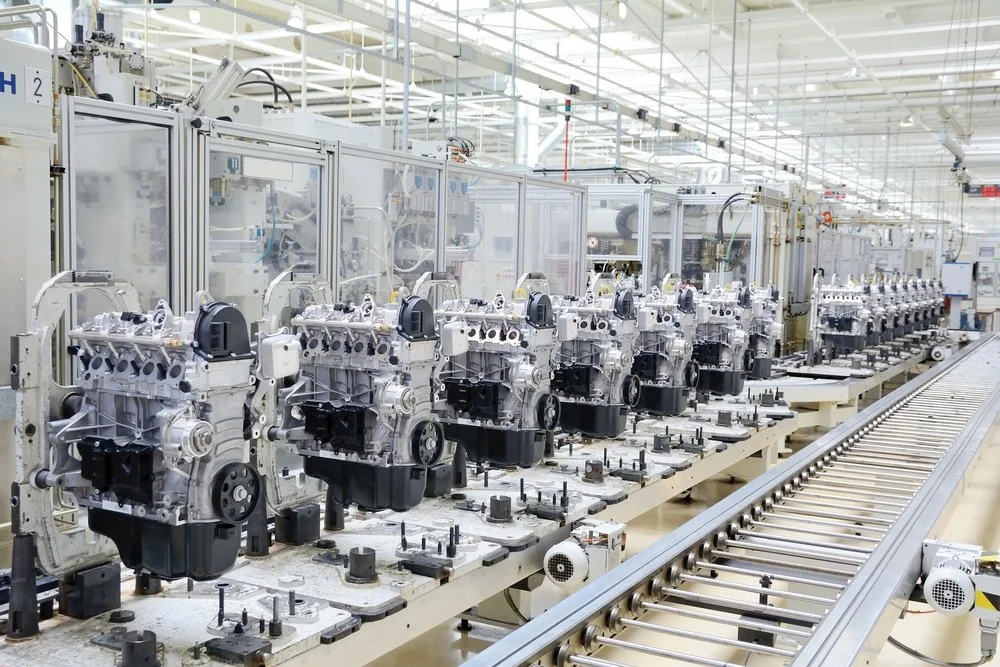

Manufacturing Equipment: Lease vs Rental vs Chattel vs CHP

Chattel mortgage is the default for most Australian manufacturers buying plant in 2026 — ownership from day one, full GST credit in the next BAS, and a clean depreciation schedule. Finance Lease, Commercial Hire Purchase and Operating Rental each have a narrow window where they beat chattel on structure, cashflow or off-balance-sheet treatment

Dandenong & South-East Manufacturer Equipment Finance (2026)

Dandenong, Hallam, Keysborough and Cranbourne read as one precinct on a credit file, not four suburbs. Here's how South-East Melbourne manufacturer equipment finance actually gets approved in 2026 — what each suburb signals to a lender, and why the March PMI softness sharpens the suburb-cluster proof pack rather than weakening it.

2026 Construction Loan Pack: Plant, Pre-Start & Dev Sequencing

The RBA cash rate sits at 4.10% after the March decision, Victoria adopts NCC 2025 from 1 May, and most builders are still stacking facilities in the wrong order. The right sequence — plant, pre-start gap, development — decides which application gets approved and which one blocks the next. Here's the 2026 construction loan pack playbook.

One Doc Home Loan for Civil Contractors: Retention Income

Civil contractors get told their retention-heavy income kills a residential application. On a One Doc home loan it doesn't — the document teardown reads BAS turnover and self-declaration, not full PAYG payslips. Here's what's actually inside the file and where the deal lives or dies.

Commercial Property Loans for Builder Owner-Occupiers (2026)

A builder buying their own yard-and-office combo isn't a residential loan, isn't a development loan, and isn't quite a standard commercial property loan either. The owner-occupier file sits in its own lane — different LVR, different servicing read, different entity structure. Here's how the file actually runs.

What Lenders See in a Low Doc Civil Plant File (2026)

A low-doc civil plant file isn't read like a vanilla asset deal. The credit team is hunting for cashflow consistency on BAS, a clean PPSR picture, supplier-invoice integrity and resale strength on the asset. Here's what's actually on the assessor's screen — and what makes the file pass on the first pass.

No Presales Development Finance: When Private Funders Say Yes

Bank development finance asks for pre-sold stock before settlement. Private and non-bank funders don't. Here's the approval anatomy of a no-presales development deal — what gets weighed, where the deal lives or dies, and why exit strategy carries the file when contracts can't.