Packaging Line & Labelling Equipment Finance (2026)

Packaging line and labelling equipment finance for food and consumer goods manufacturers – Switchboard Finance

Packaging Line & Labelling Equipment Finance (2026): The 14-Item Docs Checklist + 7-Day Approval Timeline for Food & Consumer Goods Manufacturers

Packaging and labelling equipment is rarely assessed like a simple one-machine file. Food and consumer goods manufacturers often submit deals that include imported components, conveyor sections, coding units, install costs and other line items that do not all get treated the same way by credit teams or valuers.

This page is not a broad factory finance explainer. It is a sub-niche guide that combines a document checklist and a practical first-week approval path, so you can see what usually needs to be ready before the file starts dragging into re-quotes, follow-ups or valuation friction.

- Hub (non-negotiable): Business Owners Finance Hub

- Persona hero explainer: Manufacturing Equipment Finance Melbourne: Low Doc Loans for Plant, Vehicles & Factory Upgrades

- Money page of the month (forced target): Pre-Approved Manufacturing Upgrades: Line Up Asset Finance (2025 Guide)

- Winner seed #1: Manufacturing Equipment Finance Documents Checklist (2026)

- Winner seed #2: Factory Plant Finance Approval Timeline (2026)

- Sibling post #1: Imported Machinery Finance (2026): Landed Cost vs Valuation

- Sibling post #2: Factory Upgrade Pack (2026): 12 Costs You Can Bundle Into Equipment Finance (Not Just the Machine)

- Glossary (unique, no repeats): Equipment Finance and Tax Invoice

The cleanest packaging-line files are the ones that separate the financeable equipment story from the soft-cost and timing story early. If the quote is vague, the imported components are not clearly described, or the conveyor and install pieces are bundled badly, the consequence is usually not an instant decline — it is a slower, more conditional approval path that starts filling with follow-up questions.

| Day | What usually happens | What the lender wants clean | What causes delays |

|---|---|---|---|

| Day 0–1 | Initial review and document check | Clear quote pack and entity details | Vague bundled pricing |

| Day 2–3 | Credit read and asset logic review | Supplier, asset scope and usage clarity | Too many soft-cost lines mixed in |

| Day 4–5 | Valuation or comfort checks if needed | Imported and conveyor sections itemised | Missing specs or landed-cost confusion |

| Day 6–7 | Conditions cleared and settlement prep | Final invoice path and install timing | Re-quotes, changed scope or missing proofs |

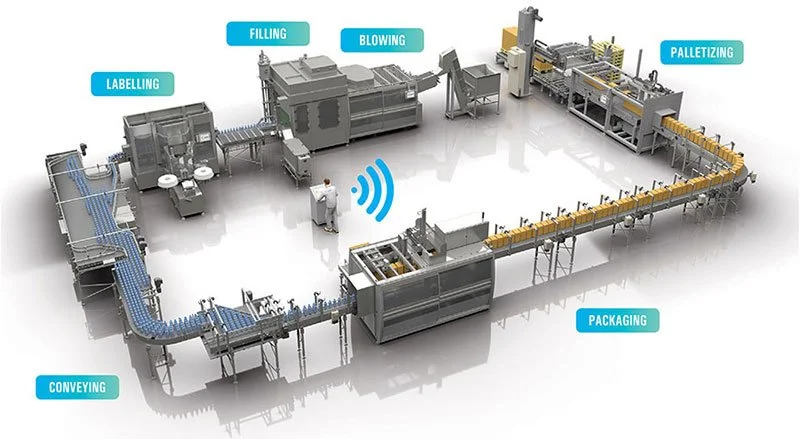

1) Why packaging and labelling lines get assessed differently

A packaging line often looks simple from the outside, but the paperwork usually says otherwise. Instead of one clean asset, the deal may include the main machine, conveyor sections, coding or printing modules, sensors, safety frames, install costs, freight, commissioning and sometimes imported parts that do not all fit neatly into one valuation story.

That is why this sub-niche behaves differently from a simple standalone plant file. If you submit it like a single-piece machine purchase, the consequence is usually confusion around what the lender is actually comfortable funding and what they want split out, clarified or treated separately.

- There is often a high soft-cost component: more non-core line items than a basic machine purchase.

- Bundled systems can be read unevenly: conveyors and add-ons are not always treated the same as the main unit.

- Import exposure can complicate timing: landed-cost and supplier clarity start mattering earlier.

A food manufacturer may think they are financing “one new packaging line,” but the quote can actually contain multiple asset buckets. If those buckets are not clearly separated, the lender often comes back with questions before the file can move cleanly.

2) The 14-item docs checklist lenders usually want first

The best packaging-line submissions are the ones that make the asset story easy to read. That means the lender can see who is buying, what is being bought, which pieces are core equipment, and which costs are support items wrapped around the project. The checklist is less about “more paperwork” and more about avoiding preventable ambiguity.

If even a few of these are missing, the consequence is usually a slower first week. The deal may still move, but it tends to move through extra follow-ups, quote revisions or clarification requests that could have been avoided at the start.

- 1. Full supplier quote with each line item clearly described

- 2. Separate identification of the main packaging unit

- 3. Separate identification of labelling, coding or printing modules

- 4. Conveyor or feed sections itemised clearly, not hidden in one lump sum

- 5. Freight or shipping shown separately where relevant

- 6. Install and commissioning costs separated from the hardware total

- 7. Manufacturer or supplier specs / model references

- 8. Buyer entity details matching the application

- 9. Director ID / signatory details where required by the lender

- 10. Recent business account evidence showing stable operating flow

- 11. Trading summary or business background for the production use-case

- 12. ABN / GST position consistent with the buyer entity

- 13. Deposit or contribution plan if part of the structure

- 14. Final invoice path or staged invoice sequence if the supplier uses deposits

A consumer-goods manufacturer can have enough commercial strength for the deal, but if the quote bundles the printer, conveyor, install and freight into one vague total, the first delay usually comes from the paperwork — not from the business itself.

3) What the first 7 days of approval usually look like

Day 0 to Day 1 is about file shape. The lender checks whether the submission is complete enough to read, whether the entity and supplier details line up, and whether the quote actually shows a financeable asset story. Day 2 to Day 3 is usually where the structure becomes clearer: the lender starts looking at the line, the business profile and whether any parts of the quote need more separation.

Day 4 to Day 7 is where slower files start showing their problems. If conveyors, imports or soft costs are unclear, this is where valuation or credit comfort questions usually appear. If the pack is clean, the same days are often used to clear conditions and line the file up for settlement. If the pack is messy, the consequence is that the “7-day” path becomes a re-quote path instead.

- Days 0–1: completeness check, quote clarity and entity match.

- Days 2–3: credit reads the asset logic and the commercial use-case.

- Days 4–5: valuation comfort tightens or clears depending on the quote detail.

- Days 6–7: conditions clear if the invoice path and scope stay stable.

Two similar packaging-line files can start on the same day. The cleaner one reaches conditions quickly because the quote is already separated properly. The slower one spends the week fixing line-item descriptions and re-issuing supplier paperwork.

4) The five packaging-line delay triggers most files miss

The biggest delay triggers are usually not dramatic. They are small drafting problems that make the lender unsure what they are actually financing. In this sub-niche, the common ones are bundled conveyor pricing, imported equipment with unclear landed-cost logic, install costs mixed into the machine value, supplier quotes that read more like proposals than invoices, and project scope changing after submission.

None of those automatically kill the deal. But they do create drag. If you ignore them, the consequence is a file that stays technically alive while becoming slower, more conditional and more annoying than it needed to be.

- Bundled conveyors: support systems can be read differently from the core machine.

- Import blur: landed cost, freight and equipment value are not clearly separated.

- Soft-cost mixing: install or commissioning is folded into the wrong bucket.

- Proposal-style quotes: the quote looks like concept pricing, not approval-ready pricing.

- Scope drift: the equipment list changes after the lender has already started assessing it.

A manufacturer may send what looks like a complete supplier pack, but if the document still reads like “draft concept pricing” rather than a settled purchase scope, the lender often pauses to make sure the file is not moving underneath them.

5) How to keep the file clean before you submit

The simplest way to keep this type of deal moving is to prepare it like a structured equipment purchase, not like a general factory project. Make the main asset obvious, keep support costs visible, and line up the supplier paperwork so the lender can see what is core equipment, what is install-related and what may need separate explanation.

If you do that early, the 7-day path is much more realistic. If you do not, the consequence is that the lender has to spend the first week unpacking the deal instead of progressing it. The approval does not slow down because the business is weak — it slows down because the file is harder to read than it should be.

- Itemise the system properly: do not hide multiple components inside one broad line.

- Separate hardware from soft costs: clearer structure usually means fewer follow-up requests.

- Stabilise the quote before submission: avoid sending a file that is still changing in real time.

A label-and-packaging upgrade can move cleanly when the supplier documents show the machine, modules, conveyors and install path clearly from the start. The same project becomes slower when the lender has to rebuild that picture from scattered paperwork.

Packaging and labelling files are rarely delayed because the concept is hard to understand. They are delayed because the paperwork does not make the asset, the soft costs and the timing easy to separate. That is why this sub-niche needs a cleaner quote pack than a simpler single-machine deal.

Start with the Business Owners Finance Hub, then work through the manufacturing corridor pages already linked above if you need to tighten the quote, shorten the first week or reduce the chance of re-quotes and valuation drag. If you skip that structure, the consequence is usually a longer approval path before anything is actually wrong with the deal.

FAQs

Quick answers on packaging-line document packs, bundled equipment and the first-week approval path.

Use the hubs to navigate, then work through the latest 8 posts from the list above.

- Same Lender vs New Lender Refinance (2026): When Loyalty Costs You More — and the Payout + Discharge Sequence That Switches Clean

- The Double-Repayment Month Trap (2026): How to Bridge Old Repayments, New Deposits and a 30-Day Revenue Lag

- Why Consolidating All Your Facilities With One Lender Gets Declined (2026): The Lender Exposure Rules — and the Split-Lender Restructure Map for 3–6 Active Loans

- Bank Statement Narration Red Flags (2026): The 12 Transaction Labels That Slow Vehicle & Equipment Approvals

- Melbourne NDIS Provider Vehicle Finance Checklist (2026): People Movers, Wheelchair Vans & the 9 Proof Items That Speed Up Low Doc Approval

- What Is LVR in Asset Finance? (2026): How Lenders Calculate Loan-to-Value Ratios for Vehicles, Equipment & Plant — 3 Scenarios Where Your LVR Changes the Deposit Before Rate Is Even Discussed

- The Harvest Window Application Plan (2026): How Mixed-Income Ag Contractors Time Ute, Light Truck & Trailer Finance Around Peak Revenue — So They're Assessed at Harvest Income, Not Off-Season

- Geelong & Bellarine Café + Hospitality Finance Checklist (2026): The Local Proof Pack for Waterfront, Tourism-Season & Industrial-Strip Venues

Newest in the Business Owners Finance Hub

Four fresh, lender-practical reads for business owners — covering imported machinery risk, factory install readiness, pricing logic and service-van fleet payout traps.

Overseas Supplier Deposit Risk (2026)

How imported machinery deals get short on settlement when lender value lands below total outlay.

Manufacturing Credit Notes Explained (2026)

Why two factory upgrades can price differently even when the machinery looks nearly identical.

Factory Install Readiness (2026)

Power, slab, access and commissioning gaps that hold plant funding up after approval.

7 Balloon & Payout Traps SME Service-Van Fleets Hit (2026)

The stagger plan that stops multiple van loans maturing in the same quarter.